since 1976

since 1976

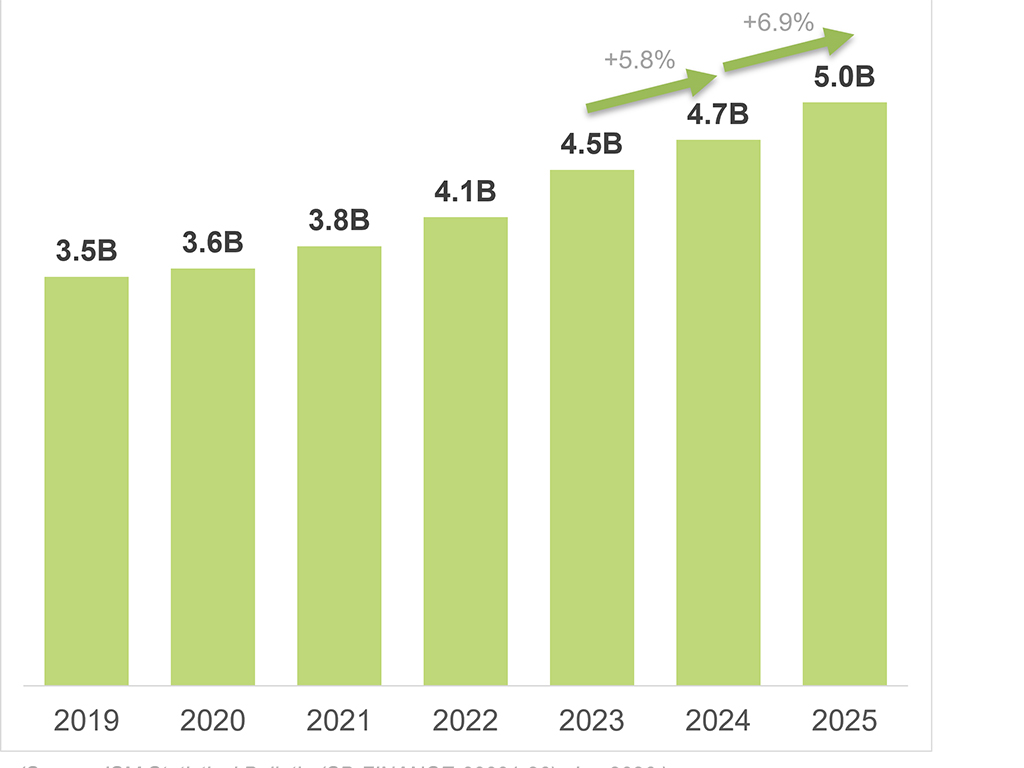

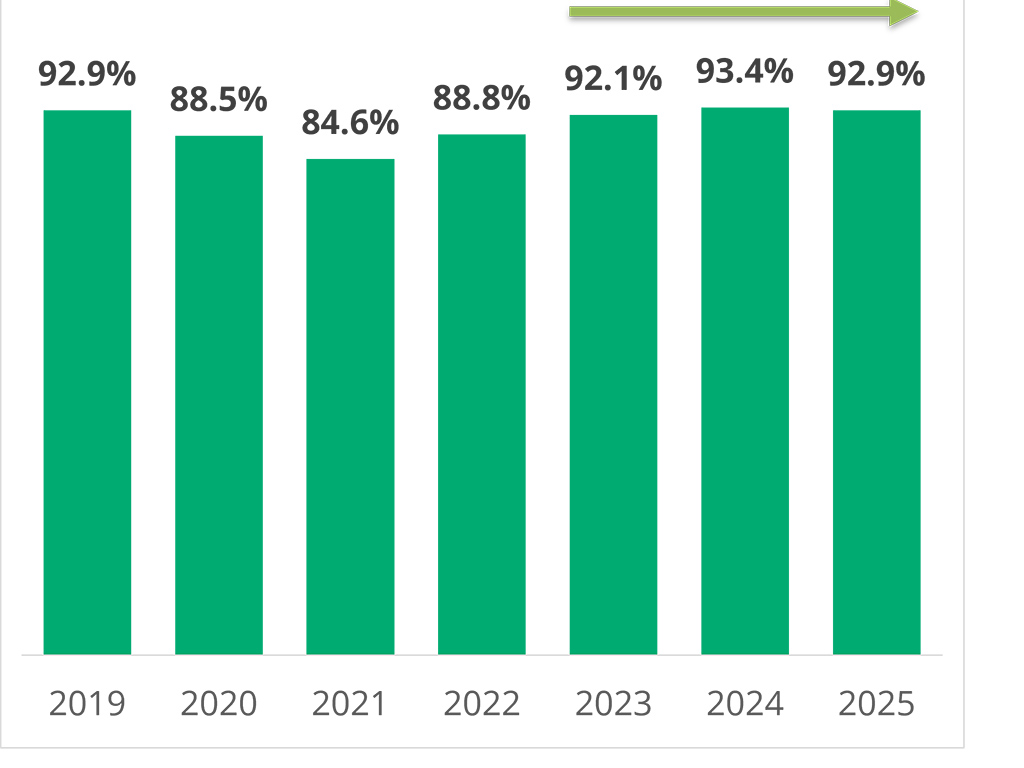

Malaysia’s general insurance industry recorded Gross Written Premium (GWP) of RM24.2 billion in 2025, a 4.8% increase from RM23.1 billion in 2024. More significantly, the industry’s underwriting profit reached RM1.2 billion; an improvement of RM125 million year-on-year with the overall Combined Ratio for underwriting results remaining around 93%.

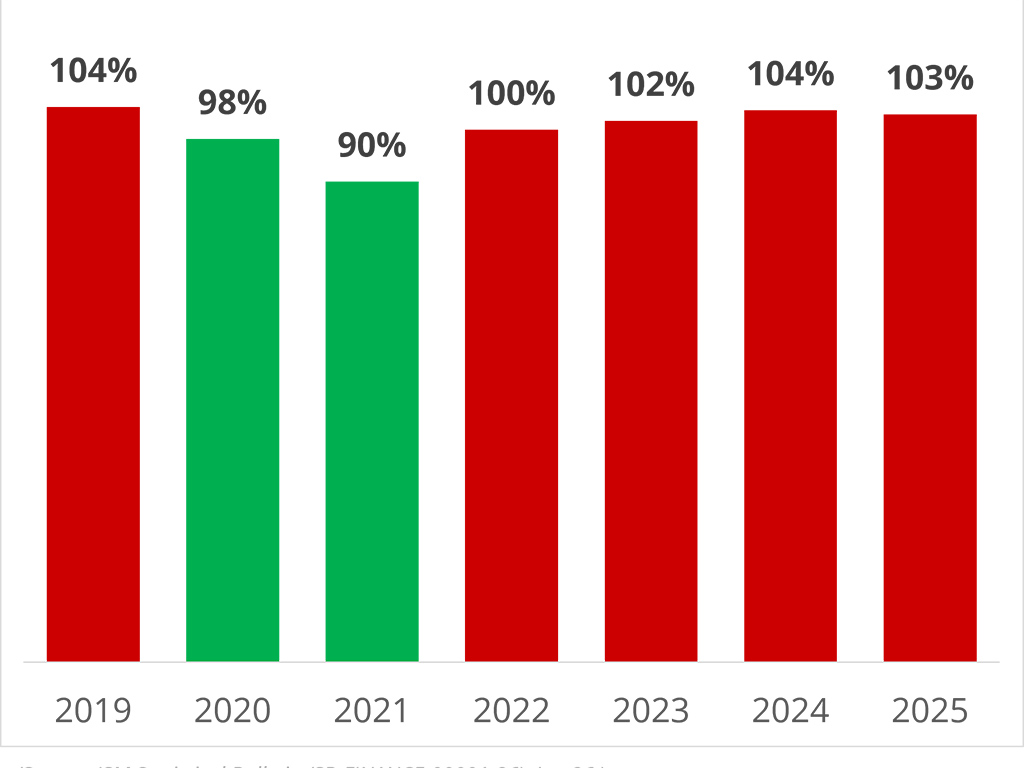

Motor insurance, which remains the general insurance industry’s largest line of business at 45.2% of total premiums, continued to register underwriting losses of RM 289.3 million, with a Combined Ratio remaining at 103%.

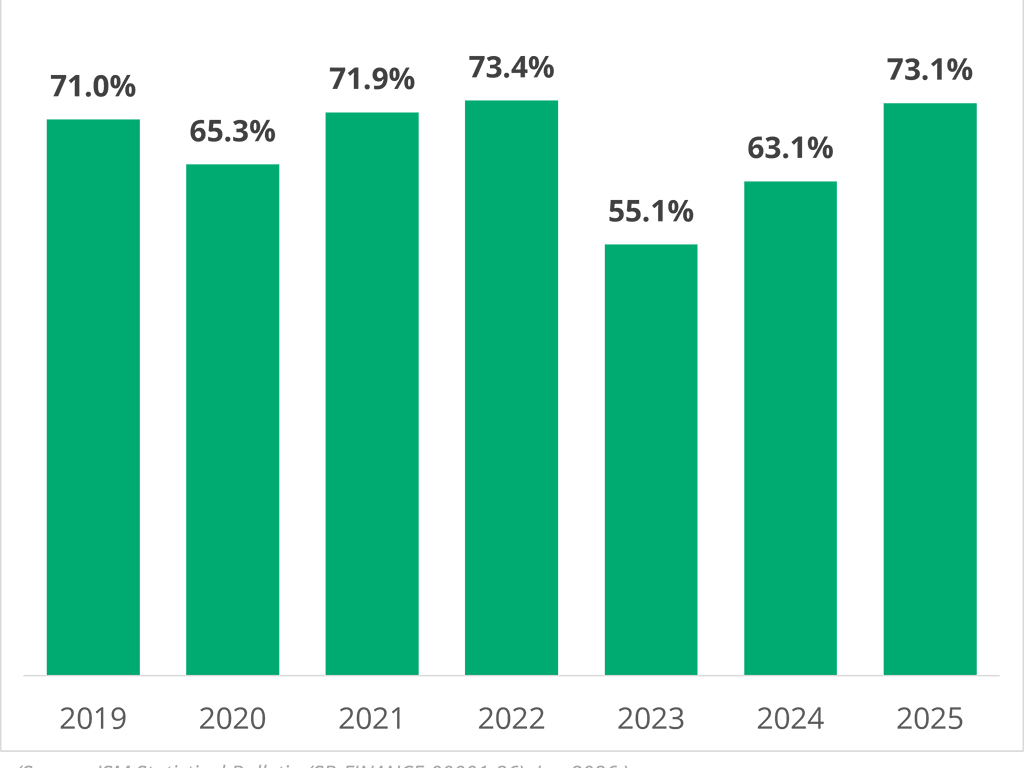

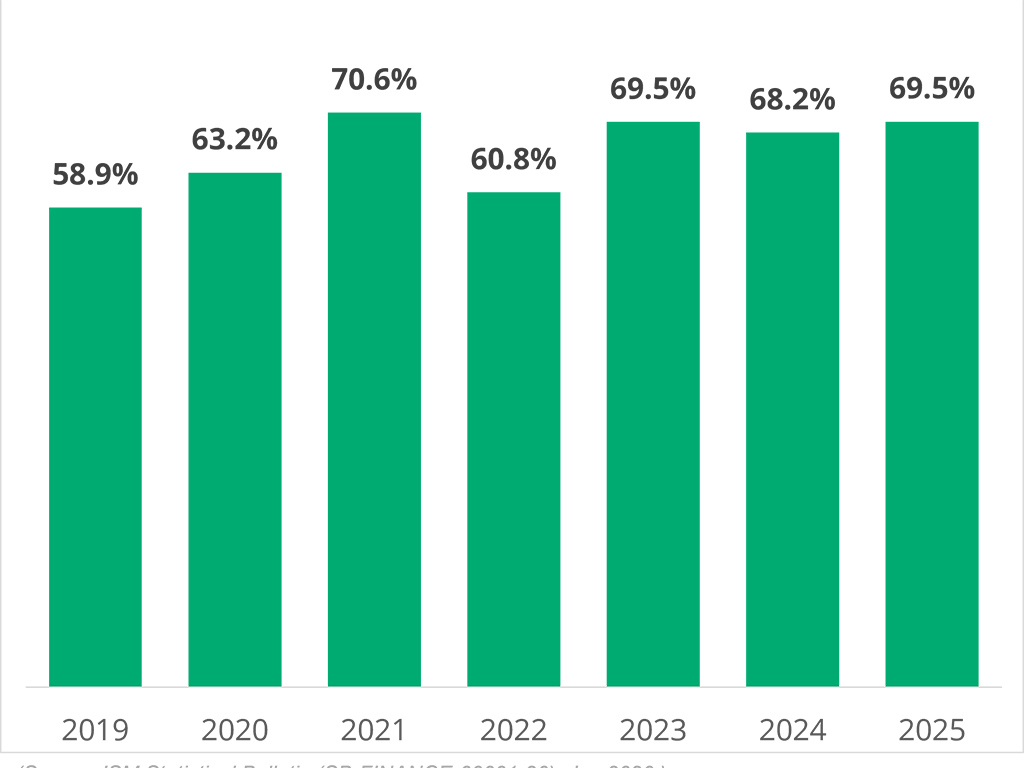

Non-motor business lines particularly Fire, Marine, Aviation & Transit (MAT) and Personal Accident (PA), contributed positively to the overall underwriting result. Fire insurance recorded an underwriting profit of RM700.8M or a Combined Ratio of 69.5%.

“The improvement in the general insurance industry’s underwriting performance is an operational milestone and reflects the sector’s ability to absorb rising claims costs while continuing to protect millions of policyholders,” said Mr. Chua Kim Soon, CEO of General Insurance Association of Malaysia or Persatuan Insurans Am Malaysia (PIAM). “As we strengthen industry resilience; our focus remains on building a well-insured nation, ensuring a faster recovery for Malaysians with their assets, livelihoods and operations safeguarded through the support of our insurers and reinsurers.

Motor and Fire Lines Remain Key Growth Drivers; PA Continues Upward Momentum

The combined performance of Motor, Fire and PA insurance lines collectively contributed to 6.1% growth in premiums for the general insurance industry in 2025:

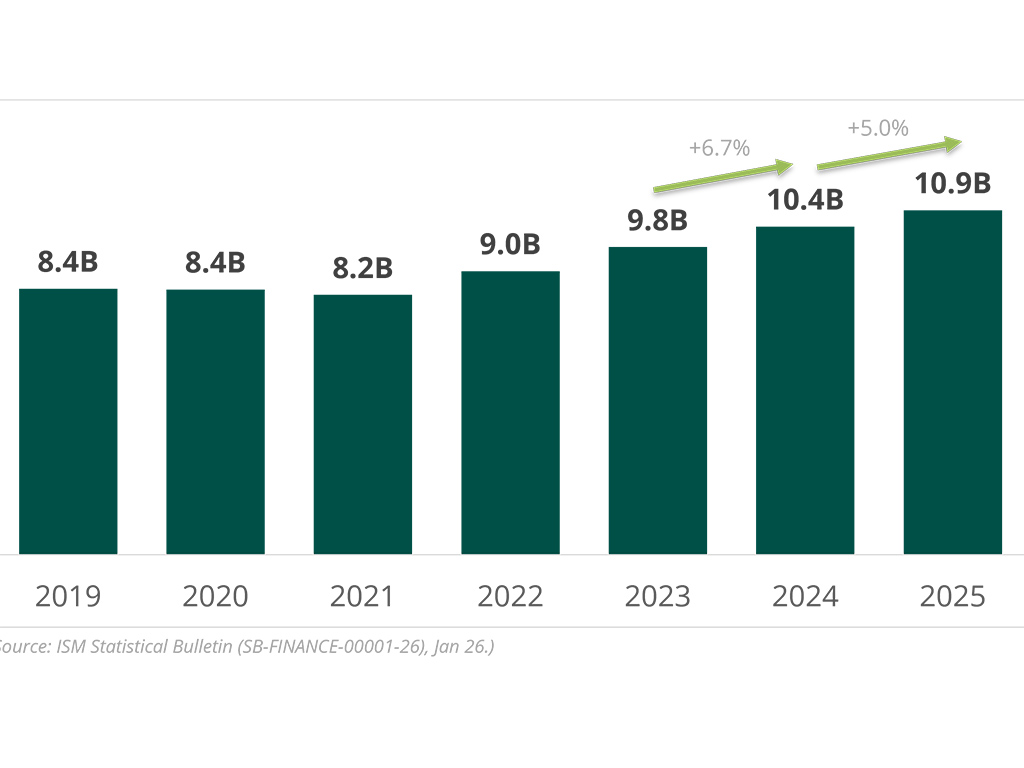

>Motor insurance remained the industry’s largest business line, contributing RM10.9 billion and representing 45.2% of the portfolio. The Motor line recorded a slower growth of 5.0% YoY in 2025 versus 6.7% in 2024.

>Fire insurance showed stronger performance and is the industry’s second largest business line, contributing RM5.0 billion and representing 20.9% of the portfolio. The Fire line recorded a stronger growth of 6.9% YoY in 2025 versus 5.8% in 2024.

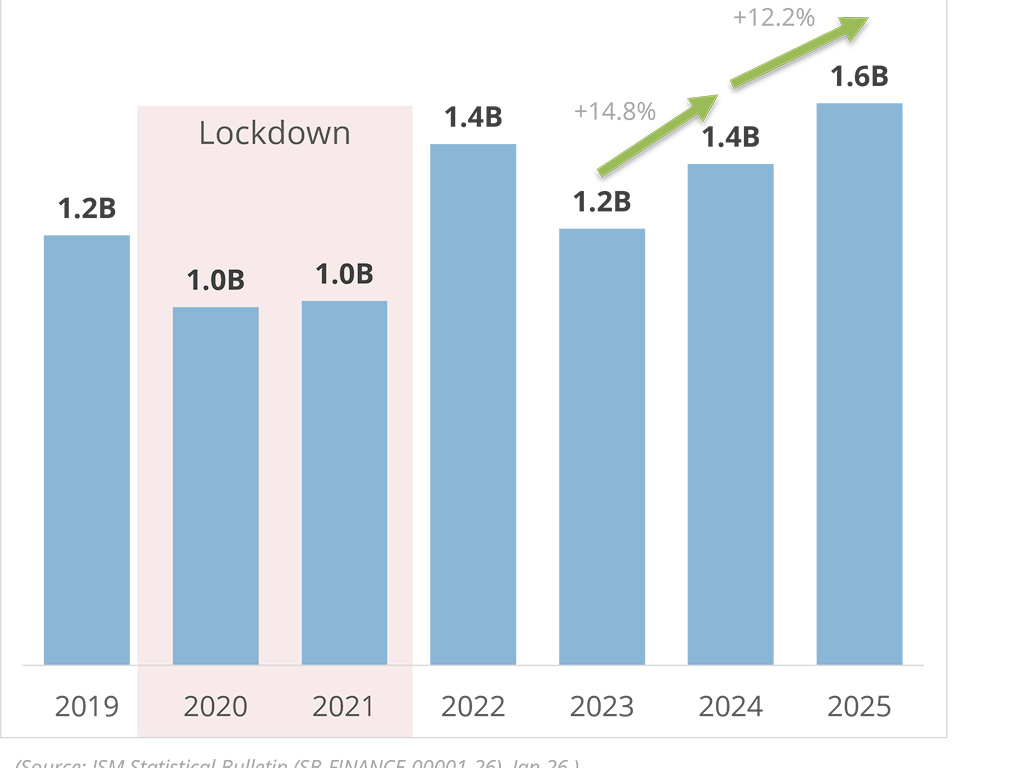

>PA insurance, a growing segment, reached RM1.6 billion in 2025 with a 12.2% growth rate. This line of business represents 6.5% of the portfolio.

Motor insurance

Motor insurance continued to operate at an underwriting loss of RM289.3 million, with a Combined Ratio of 103%. This reflects that claims payout exceeded premiums collected. The 0.7-point improvement from 2024 reflects tighter underwriting discipline, but persistent cost pressures in the Private Car segment continues to strain the shared pool that funds every policyholder's claims.

Rising claim frequency: Private Cars claim frequency maintained above 7% in 2025. As Malaysia's highest-volume vehicle segment, models such as the Proton X50 and X70 naturally show higher frequency concentrated among younger drivers in these popular segments.

Rising claim severity: Private Cars claim severity increased to RM8,831 in 2025 due to spare parts inflation, notably for Proton Saga & Proton X50.

Fire Insurance

Fire insurance grew by 6.9% from RM4.7 billion to RM5.0 billion in GWP, driven by sum-insured inflation on residential sub-sales, largely due to rising rebuild cost inflation, shifting risk exposure toward older landed homes in suburban areas. The segment reported a Combined Ratio of 69.5% and total underwriting profit of RM700.8 million.

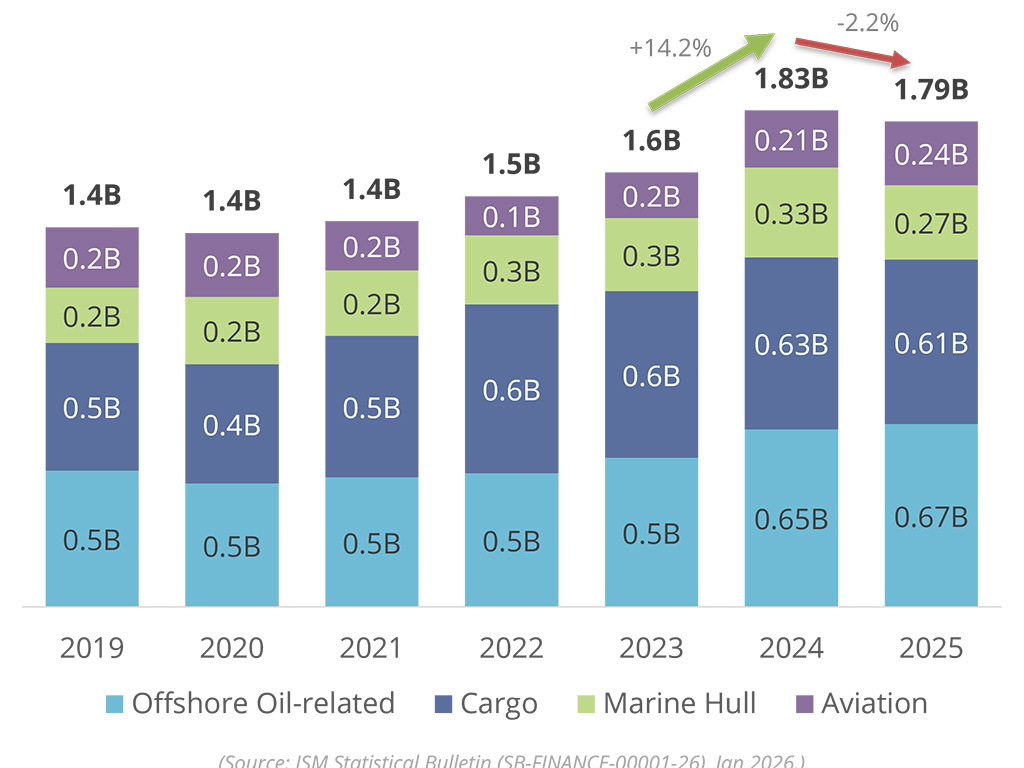

Marine, Aviation and Transit (MAT) Insurance

MAT insurance mainly consists of Offshore Oil-related and Cargo businesses, respectively contributing to 37.6% and 33.9% of the portfolio. MAT slightly dropped by 2.2% from RM1.83 billion to RM1.79 billion in GWP – moderation seen in Offshore Oil-related and Cargo segments.

This business recorded a contraction of -2.2% in 2025 while maintaining a strong underwriting profit of RM108.1 million and a Combined Ratio of 73.1%. This is lower than the recorded RM161.8 million in 2024. Cargo and Marine Hull businesses contributed 89.6% of the business.

Personal Accident Insurance

Personal Accident (PA) insurance recorded double digit growth, reaching 12.2% to RM1.6 billion in GWP from RM1.4 billion in 2024. The expansion was primarily supported by higher uptake of travel insurance, in line with the continued improvement in travel trend since 2023. Increased adoption of digital distribution channels, alongside broader economic recovery, also contributed to the uplift in GWP. Travel patterns also indicate a growing preference for destinations where the Ringgit has greater purchasing power.

Performance Snapshot

The general insurance industry delivered RM1.2 billion in underwriting profit, with a Combined Ratio of around 93%, reflecting sustained underwriting discipline that supported profitability despite claims volatility.

Insurers will continue to focus on maintaining underwriting discipline, operational efficiency, and innovation in product offerings particularly in electric vehicle (EV) coverage, climate risk solutions, and digital distribution channels to strengthen long-term resilience and competitiveness.

Resilient Industry, Shared Responsibility

The industry continues to balance growth with evolving risks through innovation, education, and collaboration.

Geopolitical factors – Global developments continue to influence operating costs and claims trends. The general insurance industry remains operationally resilient, with no immediate disruption to policyholders.

Climate risk and exposure – Increasing climate-related events highlight the need for stronger preparedness and awareness. Recent incidents have reinforced the importance of adequate coverage, including protection beyond basic fire insurance. During major flood events in the region including the Hat Yai flood in December 2025, insurers activated advisories and expedited claims support to assist affected policyholders who were stranded and their vehicles trapped in the flood.

Technology risks – Rapid advancements in vehicle technology, including electrification, digitalisation, and autonomy, are reshaping motor risk profiles. The industry is actively assessing these developments, with the 2025 Malaysian Claims Analytics Study published-on 24 April 2025.

Inflation and affordability – Cost pressures continue to influence consumer decisions, with greater price sensitivity and potential coverage adjustments. The industry remains focused on balancing affordability and sustainability through efficient claims and cost management; introduction of micro insurance through Government supported schemes such as Perlindungan Tenang Voucher 3.0 Programme, and consumer education programmes to help Malaysians understand their coverage and make informed financial decisions.

Fuel price movements – Changes in fuel prices driven by broader external market pressures, may affect operating costs in certain sectors, particularly transport-related services. To help ease and minimise service disruptions, insurers responded swiftly by introducing temporary support measures for essential service providers such as tow truck operators, including prioritised dispatch for hazardous situations, scheduled appointments for non-urgent towing, expanded use of panel workshop networks, and flexible reimbursement arrangements for affected motor policyholders who independently engage towing services. Comprehensive motor policyholders are encouraged to contact their insurer’s 24-hour assistance helpline first and verify reimbursement eligibility before arranging independent towing.

Strengthening Community Protection

Road safety education and partnerships, including collaboration with VTAREC, continue to support accident and theft reduction efforts.

Affordable protection initiatives such as Perlindungan Tenang Voucher 3.0 Programme have reached 67,946 policies; with RM2.04 million in vouchers redeemed as of 14 April 2026.

The Digital Roadside Assistance (DRA) application enhances motor claims efficiency, transparency, and consumer protection through real-time assistance, authorised towing, and digital claims submission, where applicable.

In collaboration with FINCO, the industry continues to support schools and communities in disaster-prone areas through preparedness guidance, financial protection awareness, and resilience-building initiatives.